Level funding is a type of self-insurance that uses the components of stop-loss reinsurance and claims funding to provide coverage. If you are familiar with most group insurance plans, you probably know that payments don't fluctuate and you are covered as long as you make timely payments. Level funding is similar, meaning that contributions are level for the plan year. Better still, if your plan runs well, you have the opportunity to have any surplus left in your claims fund returned. How cool is that!

As a type of self-insurance, level funded plans are governed only by a federal law known as Employee Retirement Income and Security Act (ERISA). This allows level funded plans to avoid certain (most) provisions of the Affordable Care Act, plus they don’t have to comply with a particular state’s requirement to offer a package of mandated benefits. This flexibility may help to save you money.

Sound interesting? Scroll down to learn more.

Let's set the stage.

The Affordable Care Act dramatically changed how insurance companies develop rates for each employer group. Medical underwriting can no longer be utilized for "small" employers with less than 50 employees. (In certain states beginning 1-1-2016, "small" is defined as employers with less than 100 employees.)

This means that employers with a younger or healthier employee population are now simply part of a large pool that must account for all types of health risks. Because the law also requires insurance companies to refund premiums when their loss ratios are better than allowed, (80 cents of every premium dollar must be spent on claims payment) there is little incentive for carriers to manage the overall risk of the pool. This is why level funding makes good sense. Level funding provides a tested innovative solution as a means to potentially save on healthcare expenses over the long term.

A better way for many employers.

Level funding is good for certain types of employer groups. If your employee population is relatively stable and healthy, level funding may provide cost savings as well as give the employer significantly more control. This arrangement does not guarantee immediate savings, but is designed to be a long term strategy to control the rising cost of healthcare benefits.

Conversely, if your employees are high utilizers of healthcare services, or your company experiences a high rate of employee turnover, this type of arrangement is likely not a good fit. Remember you're funding a portion of your own claims, and it's beneficial to make decisions that lead to healthy lifestyle solutions and outcomes.

Not quite sure if level funding is right for your business?

Read on. . .

What does level funding mean?

The “level” in level funding refers to the fact employers pay a level or fixed contribution each month - similar to traditional fully insured health plan premiums. There are no surprises, the fixed contribution covers everything.

Yeah, but what’s "everything?"

The level monthly contribution includes claims costs, administration fees, network access fees, the costs for the stop-loss insurance, and commissions.

How are Contributions Calculated?

Monthly contributions are based on the number of covered employees, expected claims (based upon the health risk of those employees as reported on their health risk questionnaire), the cost of stop-loss insurance, administrative fees, and commissions.

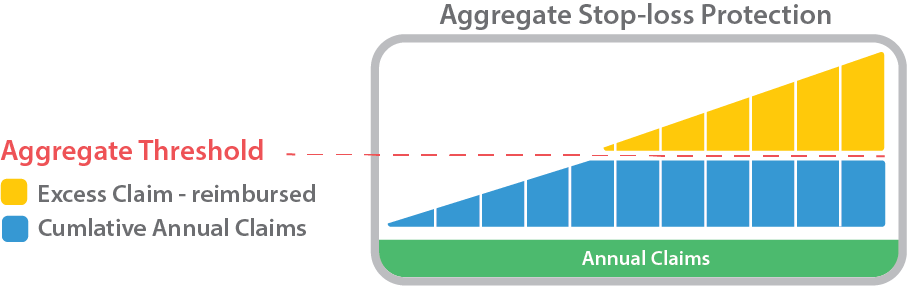

What is stop-loss insurance?

As the name implies, stop-loss insurance “stops” claims (the “loss”) from counting towards an employer’s total claims liability at certain predefined thresholds. Stop-loss coverage is a very important protection and is key to level funding.

Stop-loss insurance

Stop-loss will kick in when all claims that an employer incurs exceed the predetermined dollar amount (e.g. the claim threshold). When this happens, the stop-loss insurance carrier pays the claims on behalf of the employer.

Advanced Monthly Accommodation

No need to wait for claim reimbursement until the end of the plan year. Pacesetter's Advanced Monthly Accommodation provides for an advanced reimbursement if the employer exceeds their maximum claims liability (aggregate threshold) during the plan year. This policy feature helps smooth out cash flow for employers that pay more claims than anticipated.

Potential Savings

When actual claims are less than projected, the company receives the excess claims fund back!

If the actual claims for the plan are greater than the projected maximum claims, the company does not pay more than the projected maximum, and these excess claims are

not carried forward into the next plan year.

Choose benefit designs that work for your company.

With Pacesetter, plan designs match the specifications of the business owner and the needs of their employees. Plus, employers have the ability to choose benefit designs each plan year based on the company’s specific claims and utilization reports.

The Employer chooses from various options for deductible levels, coinsurance, co-pays and upgraded well care, and pharmacy benefits. Employers can even make their plan design compatible with tax advantaged high deductible accounts or Health Savings Accounts (HSA).

Quality provider networks.

Pacesetter provides broad access to local health care providers and facilities within our provider networks. Many employers opt to use Reference Based Pricing which allows employees to choose any doctor that accepts the Plan's referenced pricing method, which is usually a percentage based on Medicare. And, if a doctor or hospital doesn’t participate, employees can still use them, it simply costs them a bit more. Remember, the employer is funding the claims. Providers and networks - and the discounted fees they offer - are a very important component of level funding!

Meaningful Reports

Every Pacesetter client has access to meaningful reports that track exactly how claims dollars are spent. These reports can help shape benefit decisions, lead to tailored wellness offerings, and the like. Contrast this to most plans available to small employers today where there is no reporting. Often, the rates are the rates, the benefits are the benefits and employers have no control over either of them. Not true with Pacesetter.

Pacesetter Overview

• Stop Loss Coverage provided by a carrier rated “A” (Excellent) by A.M. Best or by a captive reinsured by Lloyds

• Administered by a nationally approved claims administrator

• No Lasering – First Year or Renewal

• Maximum monthly and annual contribution for the Plan Sponsor

• No claims history required to underwrite groups that are currently fully insured

• ERISA program, no state mandates

• Fully integrated cost containment

• Fully transparent rates, costs and expenses

• HSA compatible plan options

Contract Considerations

• Stop Loss Coverage

• 12/18 Contract (claims incurred in 12 month contract year and paid in contract year plus 6 months)

• Advanced Monthly Accommodation included on all accounts at no cost

Group Requirements

• Minimum of 5 Employees (possibly less depending on group and state requirements), Maximum of 150 Employees enrolled

• Employer contribution towards employee coverage must be a minimum of 50%

• True employer/employee relationship - no 1099 contractors

Medical Underwriting

Past claims history, which may not be available or is difficult to obtain from fully insured carriers, is not required for underwriting. Instead, the Employer completes an Employer Application and Group Medical Questionnaire. Employees merely complete an Employee Health Evaluation & Enrollment Form.

No "Lasering"

Upon initial rate quote or renewal, some level funding programs may place a higher deductible on certain individuals or even exclude them from coverage. NOT Pacesetter! If the group is accepted for coverage, all eligible employees are covered and all have the same benefits.

It all starts with a quote.

To get started, simply complete the contact form below, call us toll free, or contact your local broker.

What to expect next.

1. Employers provide employee census, completes an Employer Application, and a Group Medical Questionnaire

2. Employers provide information on their current plan, including rates and benefits

3. Employers review benefit plan options - this is where a broker's expertise really comes into play

4. Underwriting develops a "proposal rate quote" that is specific and unique to the employer

5. The employer accepts the proposal

6. Employees complete an online Employee Health Evaluation & Enrollment form

7. Underwriting reviews employee medical details and determines a "final rate quote"

8. Employer signs Notice of Acceptance

9. Employer executes Group Health Data form

10. Employer sends binder check

Remember, this is self-insurance and not all employer groups will qualify for coverage.